All Categories

Featured

Table of Contents

A PUAR permits you to "overfund" your insurance plan right up to line of it ending up being a Changed Endowment Contract (MEC). When you make use of a PUAR, you swiftly boost your money worth (and your survivor benefit), consequently increasing the power of your "bank". Better, the even more cash money worth you have, the greater your interest and returns payments from your insurance coverage business will certainly be.

With the rise of TikTok as an information-sharing system, economic suggestions and methods have actually found an unique method of spreading. One such technique that has actually been making the rounds is the boundless financial idea, or IBC for short, amassing endorsements from celebs like rapper Waka Flocka Flame. However, while the approach is presently prominent, its origins trace back to the 1980s when financial expert Nelson Nash presented it to the world.

Infinite Banking In Life Insurance

Within these plans, the money worth expands based on a rate established by the insurer (Infinite Banking concept). When a considerable cash money value builds up, insurance holders can acquire a money worth loan. These finances differ from conventional ones, with life insurance policy acting as security, implying one might shed their insurance coverage if loaning excessively without sufficient cash worth to support the insurance prices

And while the allure of these policies is obvious, there are innate restrictions and dangers, necessitating attentive cash money value surveillance. The approach's authenticity isn't black and white. For high-net-worth individuals or entrepreneur, particularly those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and compound growth might be appealing.

The allure of limitless financial doesn't negate its obstacles: Price: The foundational demand, a permanent life insurance plan, is more expensive than its term equivalents. Eligibility: Not everyone gets whole life insurance policy as a result of strenuous underwriting processes that can leave out those with specific health or way of life conditions. Intricacy and threat: The elaborate nature of IBC, paired with its risks, may discourage lots of, particularly when easier and much less risky choices are available.

What do I need to get started with Infinite Banking?

Designating around 10% of your regular monthly earnings to the plan is simply not feasible for many people. Making use of life insurance policy as a financial investment and liquidity resource requires self-control and tracking of plan money value. Seek advice from a financial advisor to figure out if limitless financial lines up with your concerns. Part of what you read below is merely a reiteration of what has already been said over.

Before you obtain yourself into a situation you're not prepared for, know the following first: Although the idea is frequently sold as such, you're not really taking a car loan from yourself. If that held true, you wouldn't need to settle it. Rather, you're obtaining from the insurance business and need to repay it with rate of interest.

Some social media sites messages advise utilizing cash money worth from whole life insurance policy to pay for charge card debt. The concept is that when you pay off the financing with interest, the amount will certainly be returned to your investments. Regrettably, that's not how it works. When you pay back the car loan, a section of that rate of interest mosts likely to the insurer.

For the very first numerous years, you'll be repaying the commission. This makes it exceptionally tough for your policy to gather value during this moment. Entire life insurance expenses 5 to 15 times extra than term insurance coverage. Lots of people just can not manage it. Unless you can afford to pay a couple of to several hundred dollars for the following years or even more, IBC won't work for you.

Can I use Wealth Management With Infinite Banking for my business finances?

Not everyone ought to rely solely on themselves for financial security. If you require life insurance policy, below are some useful tips to consider: Consider term life insurance coverage. These plans give insurance coverage during years with considerable financial obligations, like home loans, pupil financings, or when looking after little ones. Ensure to shop around for the very best rate.

Envision never having to stress regarding financial institution finances or high passion prices once again. That's the power of unlimited financial life insurance policy.

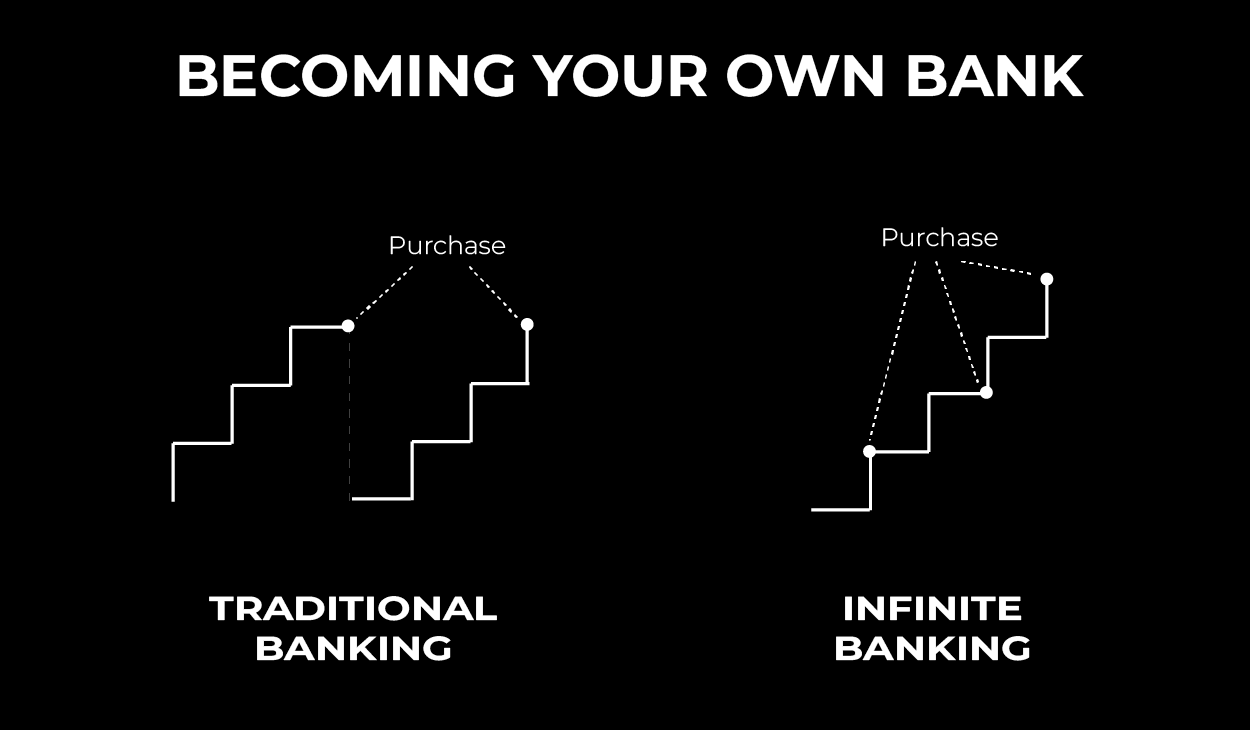

There's no collection lending term, and you have the liberty to choose the payment routine, which can be as leisurely as settling the financing at the time of fatality. Infinite Banking vs traditional banking. This flexibility includes the maintenance of the financings, where you can select interest-only settlements, maintaining the loan balance level and convenient

Holding money in an IUL repaired account being credited rate of interest can often be much better than holding the money on deposit at a bank.: You've constantly fantasized of opening your very own bakery. You can obtain from your IUL policy to cover the first expenses of leasing a space, acquiring devices, and employing staff.

What are the most successful uses of Financial Independence Through Infinite Banking?

Individual financings can be obtained from conventional banks and lending institution. Here are some vital points to consider. Bank card can supply a versatile means to obtain money for really short-term periods. Nonetheless, obtaining cash on a charge card is generally very costly with interest rate of interest (APR) commonly reaching 20% to 30% or more a year - Private banking strategies.

{kind=link}

Latest Posts

Life Rich Banking

How To Use Life Insurance As A Bank

The Concept Of Becoming Your Own Bank